Those who invested in MoneyMe (ASX:MME) a year ago are up 10%

Some MoneyMe Limited (ASX:MME) shareholders are probably rather concerned to see the share price fall 30% over the last three months. Looking on the brighter side, the stock is actually up over twelve months. But to be blunt its return of 10% fall short of what you could have got from an index fund (around 13%).

With that in mind, it's worth seeing if the company's underlying fundamentals have been the driver of long term performance, or if there are some discrepancies.

View our latest analysis for MoneyMe

MoneyMe isn't currently profitable, so most analysts would look to revenue growth to get an idea of how fast the underlying business is growing. When a company doesn't make profits, we'd generally expect to see good revenue growth. Some companies are willing to postpone profitability to grow revenue faster, but in that case one does expect good top-line growth.

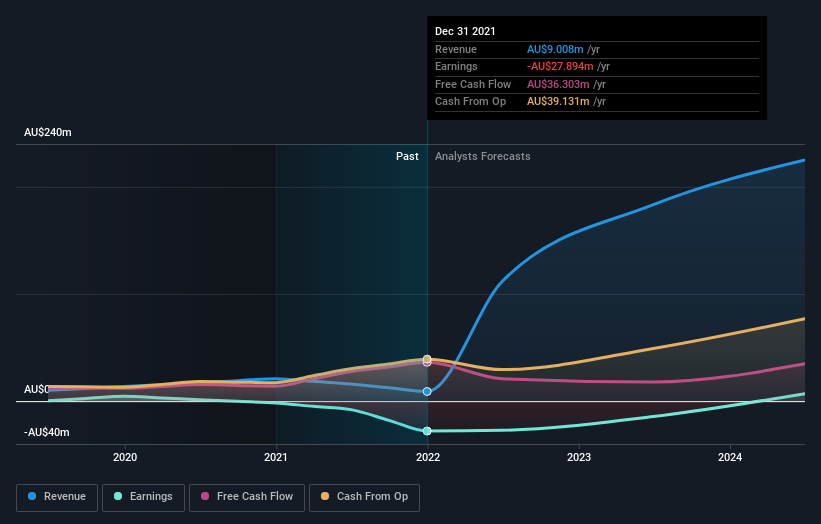

In the last year MoneyMe saw its revenue shrink by 57%. The stock is up 10% in that time, a fine performance given the revenue drop. To us that means that there isn't a lot of correlation between the past revenue performance and the share price, but a closer look at analyst forecasts and the bottom line may well explain a lot.

The company's revenue and earnings (over time) are depicted in the image below (click to see the exact numbers).

Take a more thorough look at MoneyMe's financial health with this free report on its balance sheet.

A Different Perspective

We're happy to report that MoneyMe are up 10% over the year. The bad news is that's no better than the average market return, which was roughly 13%. Unfortunately the share price is down 30% over the last quarter. It's possible that this is just a short term share price setback. If the business executes and delivers key metric growth, it could definitely be worth putting on your watchlist. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. Case in point: We've spotted 3 warning signs for MoneyMe you should be aware of.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of companies we expect will grow earnings.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on AU exchanges.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.