Yahoo Finance’s Brian Cheung contributed data to this article.

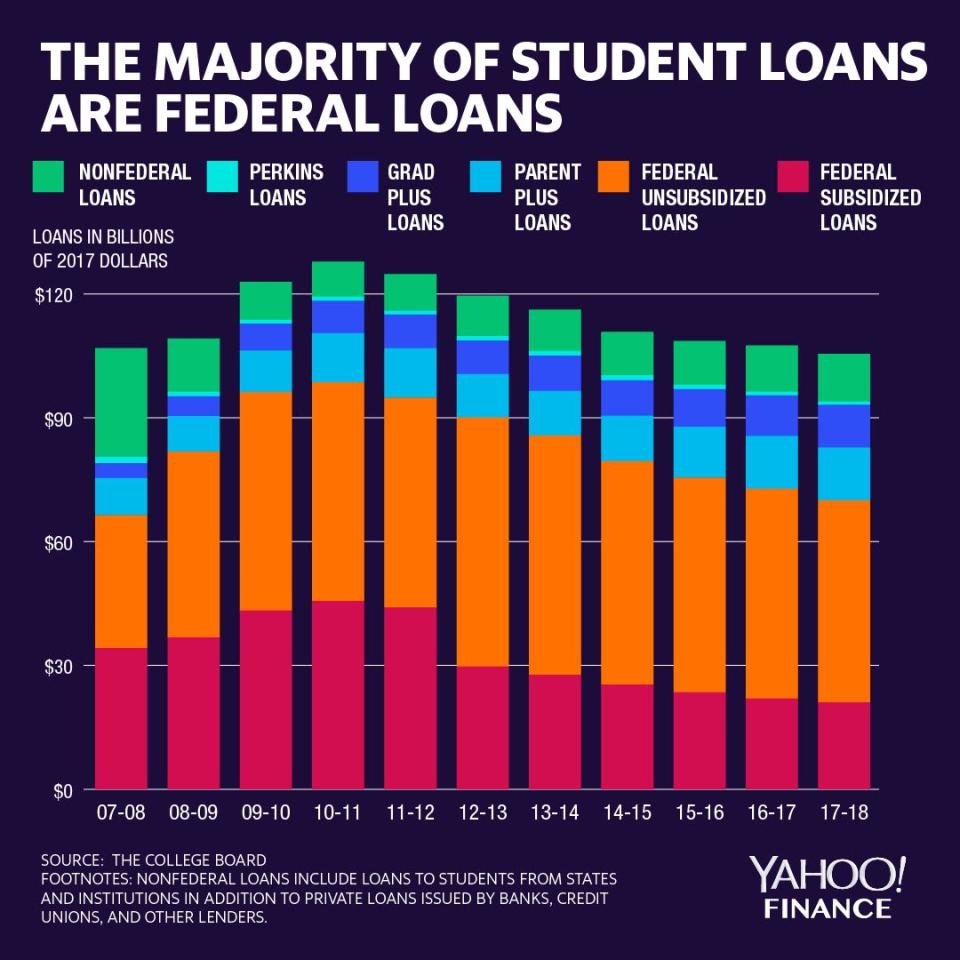

When it comes to federal student lending, the bad news just keeps coming. Federal student debt now exceeds $1.4 trillion and fully half of that is not being repaid. More than one million student borrowers default each year.

Nearly 40% are expected to default by 2023. (For context, during the financial crisis and its aftermath, mortgage delinquencies and defaults peaked at 11.5%.) Much research and study have been devoted as to why so many student borrowers aren’t paying their loans. Part of the answer may be that they never fully understood they were borrowing because of misleading marketing.

Imagine that a bank offered to help you buy a car. Let’s say that the bank sent you a letter offering a variety of different types of “aid” without clearly specifying that some of the “aid” was in the form of a loan that you would have to repay. Let’s say that the bank also didn’t disclose to you the total amount you would have to borrow to get the car or the interest rate and other key terms of the loan before you committed to its offer. Would you take the deal?

I hope not!

A lack of skepticism and regulatory oversight

Americans are somewhat wary when it comes to borrowing money from banks or other private lenders. While more can always be done to educate the public on the risks of unaffordable debt, most of us know enough to ask questions and nail down repayment terms before we commit. In addition, private lenders are subject to state and federal consumer protection laws that would never permit them to market a loan in such a misleading way.

Unfortunately, the same amount of consumer skepticism and regulatory oversight is not present when the government is the one providing that “aid” in the form of student loans. Indeed, millions of students and their families routinely commit to borrow tens of thousands of dollars from the government to finance their student’s higher education before they receive any clear disclosures of key loan terms or even understand the total amount they will likely need to borrow for the student to complete her degree.

Federal student loans are marketed around the notion that they are a benefit provided by the government to gain access to higher education, not a financial obligation. Students and their families are encouraged to make maximum use of that benefit and since it’s coming from the government, many just assume it’s in their interests to do so. Government and college websites lump loans into the category of “financial aid” along with scholarships, grants, and work study. Loans are arranged through colleges which send “award letters” to student applicants once they are accepted at a college. These letters are not subject to Truth in Lending regulation and vary widely in explaining how students will need to finance college costs. An analysis of 11,000 award letters by the New America Foundation found that less than one-third clearly distinguished debt from grants and scholarships that do not have to be repaid. A significant number didn’t even use the word “loan,” instead characterizing debt as an “award.” Perhaps this is one reason why an earlier study by Brookings found that 28% of first year student borrowers didn’t even know they had federal loans.

To their credit, the Department of Education and the Consumer Financial Protection Bureau have developed online tools to help students understand and compare the costs of attendance and their post-graduate debt obligations. However, these tools are voluntary and hampered by lack of consistency in how “aid” is disclosed in college award letters.

A trade group representing college financial aid administrators developed sample forms to better distinguish loans from other types of assistance. While an improvement, their examples still describe debt as “self-help aid,” along with work study, and permit schools to characterize the cost of attendance as “$0” even when the student is obliged to take on substantial debt to cover college costs.

Debt is a poor way to fund undergraduate education

At a minimum, the Department of Education should mandate college disclosures that clearly separate debt from other types of assistance that do not encumber students’ financial futures. Colleges should also disclose key terms such as interest costs and estimated monthly payments once the debt becomes due. Finally, they should be required to provide good faith estimates of the total debt a student will likely need to take on to complete his degree. Tuition hikes can substantially increase the amount students have to borrow each year to continue their education. A good faith estimate of the full cost of degree completion could greatly assist families in their financial planning and reduce attrition that results when students are confronted with unexpected and unaffordable tuition hikes.

Prior to 2010, federal student loans included those originated and funded by private lenders, with the government guaranteeing those lenders against student defaults. There were problems with that program and good reasons to end it in favor of direct government lending. However, one unintended consequence was the loss of the consumer protections surrounding bank lending which were enhanced with the creation of the Consumer Financial Protection Bureau in 2010. Also lost was basic expertise around credit and repayment risk, as a well-intentioned Department of Education took the lead in running the federal direct loan program. The goal of the program is to provide open access to any student aspiring to higher education. Yet, that laudable policy goal, combined with poor disclosures and misleading marketing, have led millions of student borrowers to take on obligations they never understood and cannot afford.

I have long argued that debt is a poor way to fund open access to undergraduate education. Far better would be an equity model known as income share agreements (ISAs) which base payments not on rigid amortization of principal and interest, but as an affordable percentage of what the student actually earns. Though the government has been slowly moving in that direction, it still clings to debt as the primary means of higher education finance. So long as it continues with that choice, it needs to give student borrowers the same kinds of protections and disclosures required of any private lender.

NOTE: This story was originally published and featured on Feb. 23.

—

Sheila Bair is the former Chair of the FDIC and has held senior appointments in both Republican and Democrat Administrations. She currently serves as a board member or advisor to a several companies and is a founding board member of the Volcker Alliance, a nonprofit established to rebuild trust in government.

Read more:

Former FDIC Chair: The Fed needs to hit pause on rate hikes

America has left the door wide open for bailouts

Vulnerability in America’s lower income brackets poses a risk to the economy

China thinks long-term on financial stability — so should we

Former FDIC chair: Why we shouldn’t ban bitcoin

Sheila Bair: Trump is going after the Bill of Rights

Former FDIC chair: The Fed needs to get serious about its own digital currency